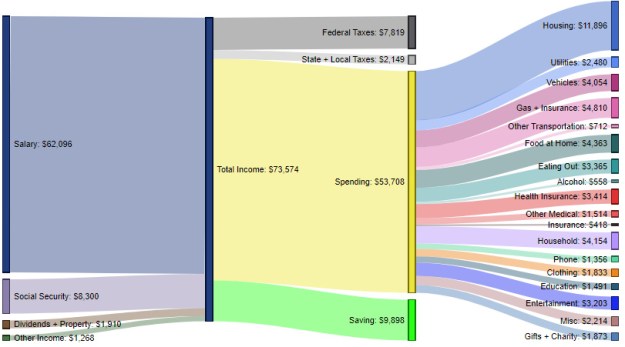

It’s tax filing time, which in our home means it’s time for the annual “How the hell did we spend so much on THAT?” ritual. Maybe that’s why I found this snapshot of how the average American household spends its money so interesting:

Source: Digg.com

Apparently, the average household has 1.3 earners, 0.6 children and 0.4 seniors, which explains why there is Social Security included in income. What I found most surprising is the health insurance number at $3,414 per year. That works out to $285.50 per month which, quite frankly, I find almost unbelievable. Here’s why:

My wife and I have been married for 27 years and for almost all of those years we’ve both worked for small companies or been self-employed. As a result, we’ve not had access to large group health insurance or, better yet, the health insurance available to government employees. If I were to make a conservative estimate, without having the numbers in front of me, I’d say that we have averaged $8,400 per year ($700/month) in health care premiums alone. Throw in co-pays and deductibles and we were almost always in the $10,000/year range.

Now, we have three kids so that obviously put us beyond the average, but health insurance isn’t necessarily linear so you can’t draw a direct corollary between the number of kids (people) and premiums. If you’d asked me to guess what the average household spent before I’d seen this data I would have said something like $5,000-$6,000 a year. That just shows how my own experience has skewed my perception of what health insurance costs, and perhaps why I felt more strongly than many of my peers that the ACA (Obamacare), as imperfect as it was, was at least an effort towards reining in the exploding costs of health insurance and health care.

As for the other numbers? Well, let’s just say this time of year also features the annual “We eat out too much” ritual self-flagellation.